We also maintain an expansive set of direct integrations across the entire digital advertising ecosystem in order to deliver our metrics to the platforms where our customers buy ads. Our partner integrations include leading programmatic platforms, such as The Trade Desk, Google Display & Video 360, Amazon, Yahoo and Xandr. Through these integrations, our customers utilize our solutions to better evaluate and optimize inventory purchase decisions. We also have direct integrations and partnerships with key social platforms, including Facebook, YouTube, TikTok, Twitter, Pinterest and Snap, as well as leading CTV platforms, including Amazon and Roku, which allow us to deliver more robust social campaign and CTV data analytics to our advertiser customers. Together, we work seamlessly to empower our partners by providing advertisers clarity and confidence in their digital investments across all key platforms.

Our Customer Interface

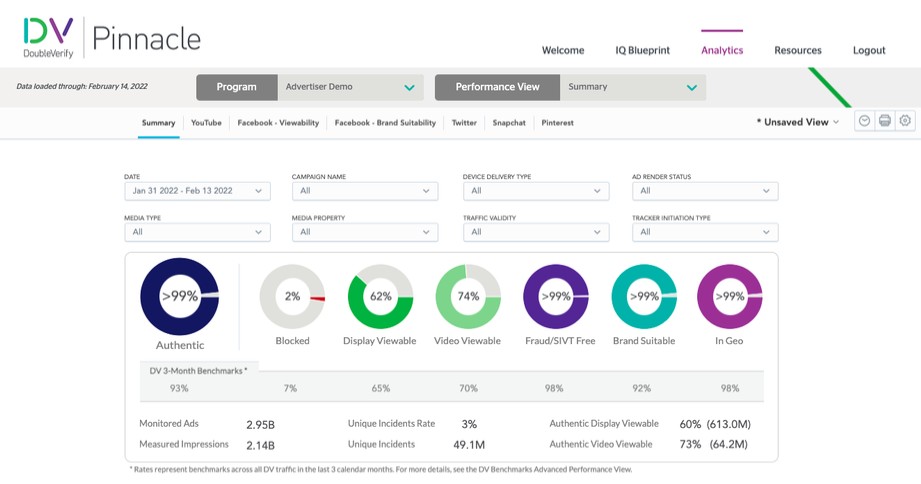

We believe our proprietary customer interface, DV Pinnacle, was the industry’s first unified service and analytics platform user interface. DV Pinnacle allows our customers to adjust and deploy controls for their media plan and track campaign performance metrics across channels, formats and devices.

Profile and Controls: DV Pinnacle allows brands to set profiles and adjust controls for their media plan’s verification settings which are then consistently and automatically deployed across all of an advertiser’s digital buying channels. Our customers use DV Pinnacle to configure their Authentic Brand Suitability settings such as inclusion/exclusion lists, override lists, custom keyword avoidance, inappropriate content avoidance categories, as well as app brand suitability controls such as filtering by app category, star reviews and age ratings. These settings are then automatically uploaded into our customers’ programmatic platforms for complete synchronicity between their pre bid and post purchase and measurement settings.

Analytics: DV Pinnacle also provides over 780 analytics and reporting metrics and over 150 industry benchmark filters in an easy-to-use dashboard, in order to track campaign performance metrics across channels, formats and devices. This enables advertisers to gain a clear understanding of the quality and effectiveness of their digital media campaigns and allows them to take appropriate actions for campaign optimization. DV Pinnacle generates industry benchmarks that are dynamically refreshed enabling customers to compare the quality of their ads against their peers and allows users to set specific thresholds on key performance indicators that drive success of the media campaign, such as blocking rates, ad delivery and viewability.

DV Pinnacle screenshot:

14